Polygon.io is Now Massive

Polygon.io is now Massive.com. The rebrand reflects our focus on scale, reliability, and continued innovation. Your APIs, accounts, and integrations continue to work without interruption.

editor

Introducing

Nov 5, 2024

In this tutorial, we'll explore a method for detecting short-lived statistical anomalies in historical US stock market data. By analyzing trading metrics, such as the number of trades executed, we can identify unusual patterns that may indicate significant market volatility events. I've been interested in this idea for a while and wanted to put forth a high-level workflow for using a simple statistical method to figure out what "normal" looks like and then quickly spot deviations.

To find these anomalies, we will download data, then we’ll build tools that not only help identify these anomalies using a lookup table, but will also provide a user-friendly web interface for exploring and visualizing them. This hands-on approach should enhance your understanding of data analysis for anomaly detection and offer an adaptable workflow.

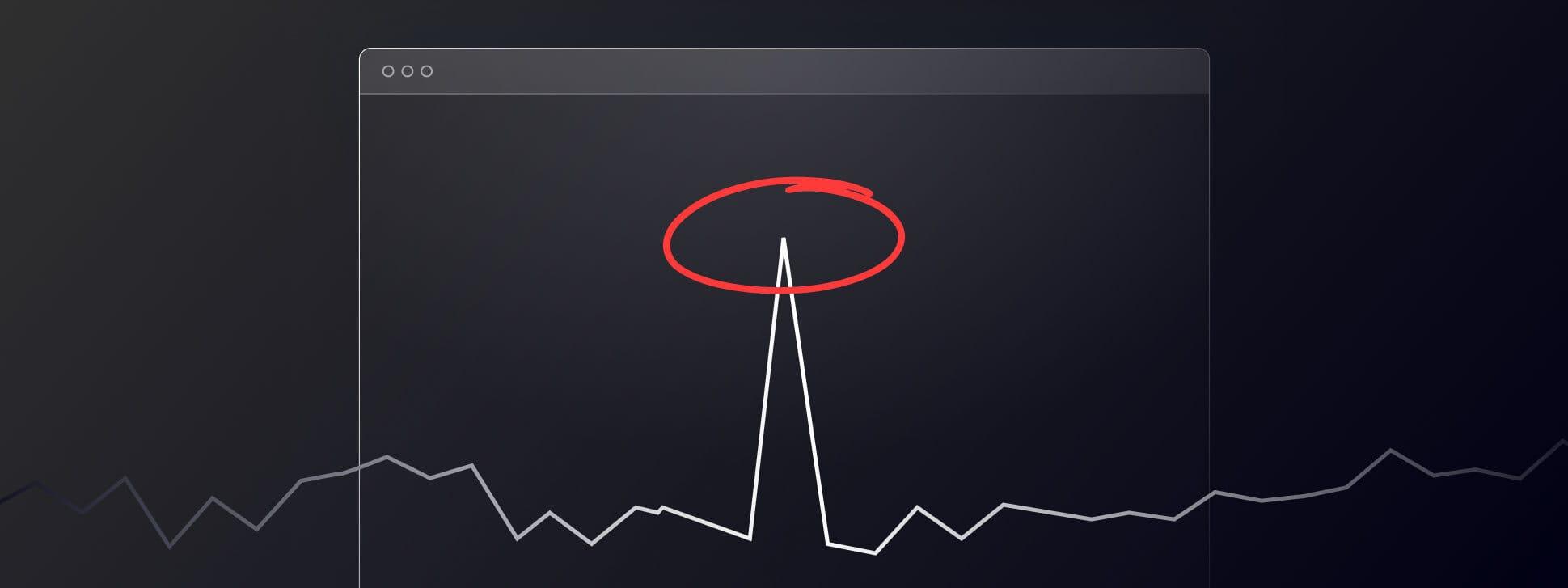

To find whether something is truly anomalous, we must first understand what "ordinary" looks like. This involves establishing a baseline or a pattern of life for a stock. This is similar to what you might have seen in a spy movie, where they have an interest in someone and start to follow them around to see what their daily routine is like. We'll do the same thing and start "following" stocks around to see what their daily routines are but at a market-wide level.

Let's look at some recent examples of detected anomalies using this method to give you a sense of what you can uncover. These examples represent some of the most significant deviations observed over the past few weeks, though as you’ll soon see many such events occur daily across the market.

Detecting anomalies is useful because sudden, short-lived deviations often indicate significant volatility events, which likely present potential trading opportunities. However, these events can also be extremely high-risk due to the unpredictable price movements since it’s easy to be on the wrong side. This tutorial focuses on the detection method and workflow for educational purposes only.

Before diving into the specifics of anomaly detection, we should probably cover the high-level workflow that guides our entire process. The steps include finding and downloading the right data, building a lookup table of pre-computed values (baselines) from the data, then querying the lookup table for deviations from the historical norms, and finally visualizing these anomalies for further analysis. This tutorial will walk you through each of these steps, ensuring you have a solid foundation for exploring stock market anomalies on your own.

There are a range of options when it comes to accessing financial data with Polygon.io: REST APIs for granular data into specific tickers, Flat Files for bulk download of market-wide historical data for things like backtesting (aggregates, trades, quotes, etc), and then real-time streaming data via WebSockets. For this tutorial, we'll focus on Flat Files because we can download many months worth of aggregated data across the entire market with just a few commands.

Before starting, you’ll need to confirm that you have an active Polygon.io subscription that includes Flat Files, or obtain an API key by signing up for a Stocks paid plan. This tutorial will use the MinIO client, compatible with S3 protocols, for managing and downloading data files from our S3 server. Detailed configuration guides for various S3 clients are available in our knowledge base article.

Download and install the MinIO client from the official page. Configure it using your polygon.io API credentials:

mc alias set s3polygon https://files.polygon.io YOUR_ACCESS_KEY YOUR_SECRET_KEY

List the available data files to understand what's accessible:

mc ls s3polygon/flatfiles/us_stocks_sip/day_aggs_v1/2024/

Download the daily aggregates for specific months you’re interested in:

mc cp --recursive s3polygon/flatfiles/us_stocks_sip/day_aggs_v1/2024/08/ ./aggregates_day/ mc cp --recursive s3polygon/flatfiles/us_stocks_sip/day_aggs_v1/2024/09/ ./aggregates_day/ mc cp --recursive s3polygon/flatfiles/us_stocks_sip/day_aggs_v1/2024/10/ ./aggregates_day/

Decompress the downloaded gzipped files for analysis:

gunzip ./aggregates_day/*.gz

We should now have all the daily aggregate CSV files uncompressed sitting in the aggregates_day/ directory. Here's as sample of what these file contain:

ticker,volume,open,close,high,low,window_start,transactions A,2797662,142.24,142.86,144.22,141.75,1722484800000000000,36394 AA,17183234,32.95,31.47,33.27,31.09,1722484800000000000,59040 AAA,4428,25.0593,25.0449,25.075,25.0301,1722484800000000000,89 AAAU,3187275,24.27,24.165,24.3411,24.08,1722484800000000000,4379 AACG,8163,0.6601,0.651,0.6612,0.651,1722484800000000000,48 AACI,106098,8.31,10.45,11.63,8.31,1722484800000000000,1309 AACIU,615,10.99,10.99,10.99,10.99,1722484800000000000,23 AACT,22655,10.745,10.745,10.75,10.74,1722484800000000000,65 AACT.WS,2040922,0.125,0.099025,0.1412,0.0754,1722484800000000000,220

Having downloaded the historical data, the next section will walk you through building a lookup table of pre-computed values based on this historical data.

In this section, we use Python, along with the

This method leverages a concept akin to hash tables in verification systems, where values are pre-computed for fast retrieval. We apply this to financial data to discern normal trading activity from short-term volatility spikes, which could indicate market anomalies. The code for all of the examples is located in this github repo.

Here’s the python

import os import pandas as pd from collections import defaultdict import pickle import json # Directory containing the daily CSV files data_dir = './aggregates_day/' # Initialize a dictionary to hold trades data trades_data = defaultdict(list) # List all CSV files in the directory files = sorted([f for f in os.listdir(data_dir) if f.endswith('.csv')]) print("Starting to process files...") # Process each file (assuming files are named in order) for file in files: print(f"Processing {file}") file_path = os.path.join(data_dir, file) df = pd.read_csv(file_path) # For each stock, store the date and relevant data for _, row in df.iterrows(): ticker = row['ticker'] date = pd.to_datetime(row['window_start'], unit='ns').date() trades = row['transactions'] close_price = row['close'] # Ensure 'close' column exists in your CSV trades_data[ticker].append({ 'date': date, 'trades': trades, 'close_price': close_price }) print("Finished processing files.") print("Building lookup table...") # Now, build the lookup table with rolling averages and percentage price change lookup_table = defaultdict(dict) # Nested dict: ticker -> date -> stats for ticker, records in trades_data.items(): # Convert records to DataFrame df_ticker = pd.DataFrame(records) # Sort records by date df_ticker.sort_values('date', inplace=True) df_ticker.set_index('date', inplace=True) # Calculate the percentage change in close_price df_ticker['price_diff'] = df_ticker['close_price'].pct_change() * 100 # Multiply by 100 for percentage # Shift trades to exclude the current day from rolling calculations df_ticker['trades_shifted'] = df_ticker['trades'].shift(1) # Calculate rolling average and standard deviation over the previous 5 days df_ticker['avg_trades'] = df_ticker['trades_shifted'].rolling(window=5).mean() df_ticker['std_trades'] = df_ticker['trades_shifted'].rolling(window=5).std() # Store the data in the lookup table for date, row in df_ticker.iterrows(): # Convert date to string for JSON serialization date_str = date.strftime('%Y-%m-%d') # Ensure rolling stats are available if pd.notnull(row['avg_trades']) and pd.notnull(row['std_trades']): lookup_table[ticker][date_str] = { 'trades': row['trades'], 'close_price': row['close_price'], 'price_diff': row['price_diff'], 'avg_trades': row['avg_trades'], 'std_trades': row['std_trades'] } else: # Store data without rolling stats if not enough data points lookup_table[ticker][date_str] = { 'trades': row['trades'], 'close_price': row['close_price'], 'price_diff': row['price_diff'], 'avg_trades': None, 'std_trades': None } print("Lookup table built successfully.") # Convert defaultdict to regular dict for JSON serialization lookup_table = {k: v for k, v in lookup_table.items()} # Save the lookup table to a JSON file with open('lookup_table.json', 'w') as f: json.dump(lookup_table, f, indent=4) print("Lookup table saved to 'lookup_table.json'.") # Save the lookup table to a file for later use with open('lookup_table.pkl', 'wb') as f: pickle.dump(lookup_table, f) print("Lookup table saved to 'lookup_table.pkl'.")

Here’s what running the script looks like:

$ python3 build-lookup-table.py Starting to process files... Processing 2024-08-01.csv Processing 2024-08-02.csv … Processing 2024-10-17.csv Processing 2024-10-18.csv Finished processing files. Building lookup table... Lookup table built successfully. Lookup table saved to 'lookup_table.pkl'. $ du -h lookup_table.pkl 80M lookup_table.pkl

This script processes the downloaded stock market data and builds a lookup table that, for each ticker, stores the pre-computed average number of trades and the standard deviation over the past 5 trading days, in a rolling window. This lets us quickly find short-lived anomalies in the data across the entire US stock market.

Now, let's leverage the power of our pre-built lookup table to query anomalies without needing the original source data. This approach significantly enhances performance, since querying the lookup table provides an extremely fast method to quickly look through large amounts of historical data and detect anomalies for each trading day. By leveraging this method, we bypass the time-consuming data processing steps and jump straight to analyzing potential market anomalies, making our analysis both faster and more scalable even for real-time detection. The code for all of the examples is located in this github repo.

Here’s the python

import pickle import argparse # Parse command-line arguments parser = argparse.ArgumentParser(description='Anomaly Detection Script') parser.add_argument('date', type=str, help='Target date in YYYY-MM-DD format') args = parser.parse_args() # Load the lookup_table with open('lookup_table.pkl', 'rb') as f: lookup_table = pickle.load(f) # Threshold for considering an anomaly (e.g., 3 standard deviations) threshold_multiplier = 3 # Date for which we want to find anomalies target_date_str = args.date # List to store anomalies anomalies = [] # Iterate over all tickers in the lookup table for ticker, date_data in lookup_table.items(): if target_date_str in date_data: data = date_data[target_date_str] trades = data['trades'] avg_trades = data['avg_trades'] std_trades = data['std_trades'] if ( avg_trades is not None and std_trades is not None and std_trades > 0 ): z_score = (trades - avg_trades) / std_trades if z_score > threshold_multiplier: anomalies.append({ 'ticker': ticker, 'date': target_date_str, 'trades': trades, 'avg_trades': avg_trades, 'std_trades': std_trades, 'z_score': z_score, 'close_price': data['close_price'], 'price_diff': data['price_diff'] }) # Sort anomalies by trades in descending order anomalies.sort(key=lambda x: x['trades'], reverse=True) # Print the anomalies with aligned columns print(f"\nAnomalies Found for {target_date_str}:\n") print(f"{'Ticker':<10}{'Trades':>10}{'Avg Trades':>15}{'Std Dev':>10}{'Z-score':>10}{'Close Price':>12}{'Price Diff':>12}") print("-" * 91) for anomaly in anomalies: print( f"{anomaly['ticker']:<10}" f"{anomaly['trades']:>10.0f}" f"{anomaly['avg_trades']:>15.2f}" f"{anomaly['std_trades']:>10.2f}" f"{anomaly['z_score']:>10.2f}" f"{anomaly['close_price']:>12.2f}" f"{anomaly['price_diff']:>12.2f}" )

To analyze a specific date's data for anomalies, run the script with the date as an argument:

$ python3 query-lookup-table.py 2024-10-18

You can also pipe the data into a file like this:

$ python3 query-lookup-table.py 2024-10-18 > 2024-10-18.txt

The output lists stocks where the number of trades on the specified date significantly exceeded the norm, indicating potential market events or anomalies.

Anomalies Found for 2024-10-18: Ticker Trades Avg Trades Std Dev Z-score Close Price Price Diff ------------------------------------------------------------------------------------------- VTAK 460548 6291.40 12387.12 36.67 0.91 106.49 PEGY 387360 15769.40 10026.18 37.06 8.15 47.91 NFLX 378687 125174.00 66580.70 3.81 763.89 11.09 JDZG 348468 37128.60 48356.15 6.44 2.09 22.94 CVS 309745 89486.00 25237.53 8.73 60.34 -5.23 HEPS 215693 1988.60 684.85 312.04 3.51 59.55 EFSH 188632 2416.40 2782.17 66.93 5.26 198.76 SLB 162587 79685.60 16971.32 4.88 41.92 -4.71 IONQ 160601 103573.60 16778.08 3.40 13.30 6.40 BIVI 159263 660.80 156.14 1015.78 2.35 109.82 ...

Having queried the lookup table, we've successfully identified a list of anomalies based on specific criteria set for trading volumes. Now we can find potentially interesting market events or anomalies, yet the output merely lists these anomalies without letting us really see them. To fix this, the next section will introduce a web interface that overlays our lookup table. This tool enables us to select a specific day and then visually explore the detected anomalies events through aggregated candlestick data, hopefully providing a more intuitive understanding of the event by looking at the trading activity.

To enhance the interactivity of our anomaly detection analysis tutorial, we have created a simple browser-based tool so that you can explore these anomalies directly through your web browser. This interface takes the next step and downloads the aggregated bars for the specific anomaly so that you can get a sense of what was happening.

Before launching the interface, ensure you have the following:

To start exploring the anomalies, run the interface script on your local machine:

python3 gui-lookup-table.py

After initiating the script, connect to the following URL in your web browser:

http://localhost:8888

The interface automatically loads the trading data for the last day seen, and you can navigate through time just as you would at the command line by specifying a date using the next and previous buttons. This feature allows you to explore anomalies over different days without manually altering script parameters.

Detected anomalies for the displayed date are listed within the interface. You can select any anomaly to delve deeper into its specifics. Upon selection, the interface will display an aggregated bar chart resembling candlestick charts used in financial analysis. This chart visually represents the trading activity of the day, highlighting the high, low, open, and close prices which can help you visually see what happened during that trading session.

The browser-based interface provides a hands-on way to visually compare and analyze the anomalies. By clicking through different dates and tickers, you can view detailed trading data including volume, price movements, and more. This visual representation aids in understanding the scale and impact of each anomaly, offering insights that are not easily discernible from raw data alone.

While this part of the tutorial does not dive into the specific coding details of the interface since it is a few hundred lines of code, it's important to note that the interface runs locally on your machine. It uses the pre-computed lookup table we built and accesses the Polygon.io API to dynamically provide aggregate bars for the ticker and date in question.

In this tutorial, we've explored the process of detecting short-lived anomalies in the stock market using polygon.io's extensive historical data with Flat Files. By downloading data, constructing a lookup table for rapid analysis, and employing a browser-based interface for interactive visualization, we've established a comprehensive workflow that not only identifies but also helps understand market anomalies.

Happy Anomaly Hunting!

Justin

editor

See what's happening at polygon.io

Polygon.io is now Massive.com. The rebrand reflects our focus on scale, reliability, and continued innovation. Your APIs, accounts, and integrations continue to work without interruption.

editor

Effective Nov 3, 2025, bid_size/ask_size will be reported in shares (not round lots) across Stocks Quotes REST API, WebSocket, and Flat Files, per SEC MDI rules. The rule is forward-looking and we’ll also backfill history for consistency. Most users need no changes.

editor

Learn how to use Massive's MCP server inside of a Pydantic AI agentic workflow, alongside Anthropic's Claude 4 and the Rich Python library.

alexnovotny